July 2026

Lubbock's economy continues to show strong retail sales growth.

Building activity has been good, led by commercial construction, while single-family residential activity remains modest. Tourism is up, and both new and used car sales are holding steady. Employment remains steady, although the unemployment rate is up from last year. Inflation related to the war and the need for moisture are factors that could have a future impact.

YTD retail sales are up 7%, while June 2026 sales increased 5% compared with June 2025. New and used vehicle sales declined slightly over the same period.

Hotel/motel tax collections continued to rise sharply in June 2026, increasing 45% from June 2025, driven in part by summer orientation at local universities.

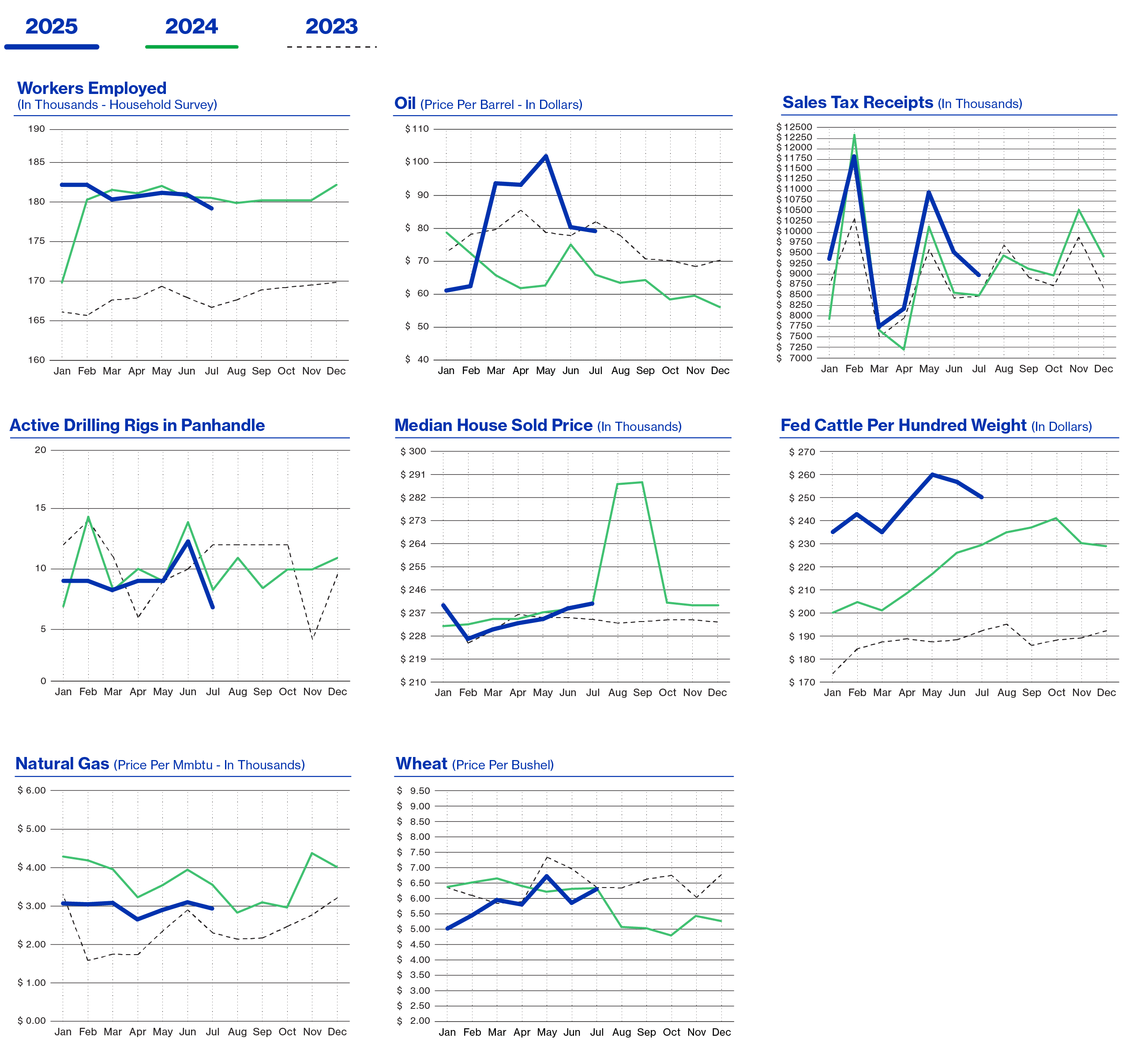

Employment in Lubbock increased slightly compared with last June, while the labor force grew 1% from June 2025. The unemployment rate rose to 4.5%, up from 3.8% a year ago, and wages increased 9% over the same period.

Mortgage rates, at nearly 7%, are higher than this time last year. However, residential permitting activity increased sharply, up 45% from June 2025. Median home prices remained steady compared with the same period last year.

Total residential activity declined YTD by $63 million, or 18%, while single-family residential activity declined YTD by $4 million, or 2%. Last year, a $67 million student housing project accounted for the difference. MTD activity in both total residential and single-family residential increased by $14 million, or 42%, compared with last year.

Total building activity is up YTD by $36 million, or 7%, driven by commercial building activity from prior months. There were no new commercial building activity in June. For the year, commercial building activity is up $99 million, or 54%, while residential building activity is down $63 million, or 18%, YTD.

YTD energy markets were mixed, with oil prices up 20% and natural gas prices down 18%.

Agricultural commodity prices also varied, with cotton prices increasing 15%, cattle prices up 10%, and milk prices down 10%. Agricultural production remains dependent on moisture and moderate temperatures. Cotton crops are mixed throughout the South Plains, with some areas reporting good crop conditions while areas with less rainfall are not performing as well.

Economic Pulse

| Economic Components | Current Month | Last Month | Last Year |

|---|---|---|---|

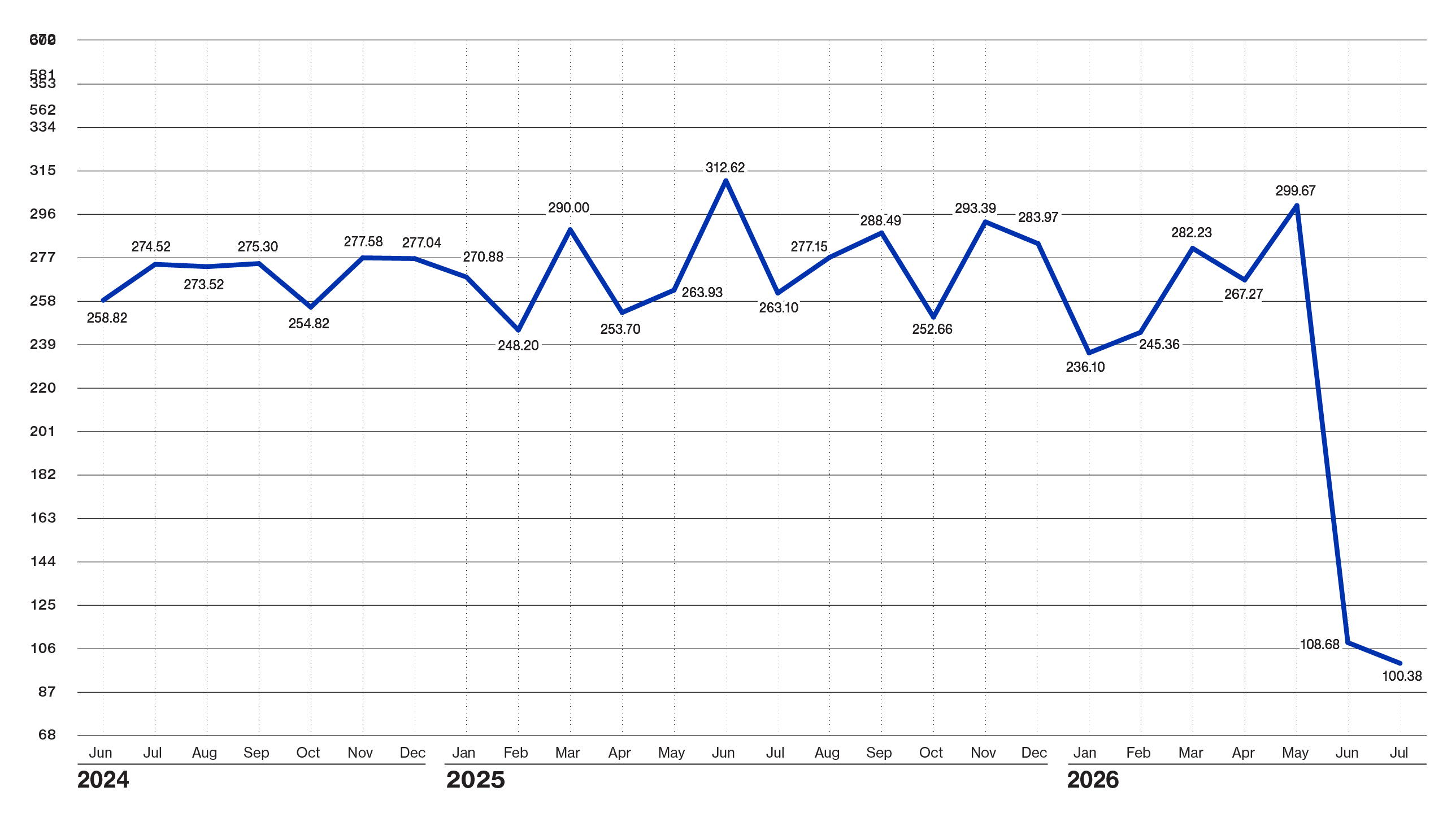

| Index (Base Jan. 88 @ 100) | $ 100.38 | $ 108.68 | $ 263.10 |

| Sales Tax Collections | $ 8,944,843 | $ 9,515,696 | $ 8,499,730 |

| Sales Tax Collection-YTD | $ 66,543,742 | $ 57,598,899 | $ 62,366,923 |

| New Vehicle Sales | 982 | 1,086 | 984 |

| Used Vehicle Sales | 1,795 | 2,044 | 1,838 |

| Airline Boardings | 50,128 | 53,532 | 50,923 |

| Hotel/Motel Receipt Tax | $ 1,104,939 | $ 1,121,233 | $ 761,329 |

| Population | 272,086 | 272,086 | 272,086 |

| Employment - CLF | 187,653 | 187,955 | 186,600 |

| Unemployment Rate | % 4.50 | % 3.60 | % 3.80 |

| Total Workers Employed (Household Survey) | 179,251 | 181,184 | 179,563 |

| Total Workers Employed (Employers Survey) | 176,500 | 177,100 | 174,700 |

| Average Weekly Wages | $ 1,143.00 | $ 1,143.00 | $ 1,044.00 |

| Gas | 79,501 | 79,720 | 79,245 |

| Interest Rates: 30 Year Mortgage Rates | % 6.625 | % 6.375 | % 6.500 |

| Building Permits Dollar Amount | $ 57,956,218 | $ 132,533,587 | $ 111,425,636 |

| Year to Date Permits | $ 581,787,974 | $ 523,831,756 | $ 546,140,508 |

| Residential Starts | 141 | 74 | 97 |

| Year To Date Starts | 787 | 646 | 828 |

| Median House Sold Price | $ 240,000 | $ 238,987 | $ 240,000 |

| Drilling Rigs In Panhandle | 7 | 13 | 8 |

| Oil Price Per Barrel | $ 79.26 | $ 80.54 | $ 66.15 |

| Natural Gas | $ 2.91 | $ 3.11 | $ 3.54 |

| Wheat Per Bushel | $ 6.39 | $ 5.83 | $ 5.34 |

| Fed Cattle Per CWT | $ 250.00 | $ 257.00 | $ 228.00 |

| Corn Per Bushel | $ 4.56 | $ 4.66 | $ 4.06 |

| Cotton (Cents Per Pound) | $ 73.07 | $ 70.43 | $ 63.75 |

| Milk | $ 15.73 | $ 15.98 | $ 17.50 |

Prepare for the majestic dance of disclaimers!

This document was prepared by Lubbock National Bank on behalf of itself for distribution in Lubbock, Texas and is provided for informational purposes only. The information, opinions, estimates and forecasts contained herein relate to specific dates and are subject to change without notice due to market and other fluctuations. The information, opinions, estimates and forecasts contained in this document have been gathered or obtained from public sources believed to be accurate, complete and/or correct. The information and observations contained herein are solely statements of opinion and not statements of fact or recommendations to purchase, sell or make any other investment decisions.

Economic Pulse Charts

{beginAccordion h3}

2026 Economic Analysis

{endAccordion}

{beginAccordion h3}

2025 Economic Analysis

{endAccordion}

{beginAccordion h3}

2024 Economic Analysis

{endAccordion}

{beginAccordion h3}

2023 Economic Analysis

{endAccordion}